Why Mortgage Rates Follow the 10-Year Treasury and Not the Federal Reserve Rate

…and Why Mortgage Rates Rose After the October 2025 Fed Cut.

If you’ve been following the headlines, you probably saw the Federal Reserve cut short-term interest rates by another .25% in October 2025. And if you’re thinking, “Great! That must mean mortgage rates dropped too!” - you’re not alone.

But the reality? Mortgage rates actually went up - by about 20 basis points (~0.20%) that same day.

So what gives? Let’s break down why mortgage rates move the way they do, why they don’t follow the Fed rate, and what last week’s rate action tells us about the market.

First, What Exactly Is the Fed Rate?

The Federal Funds Rate is the short-term interest rate banks charge each other for overnight lending. It influences:

Credit card rates

Auto loans

Home equity lines (HELOCs)

Short-term business loans

It does not directly set mortgage rates. The Fed rate affects overnight borrowing - but with 90% of US mortgages being 30 years, they are long-term investments, and that’s why…

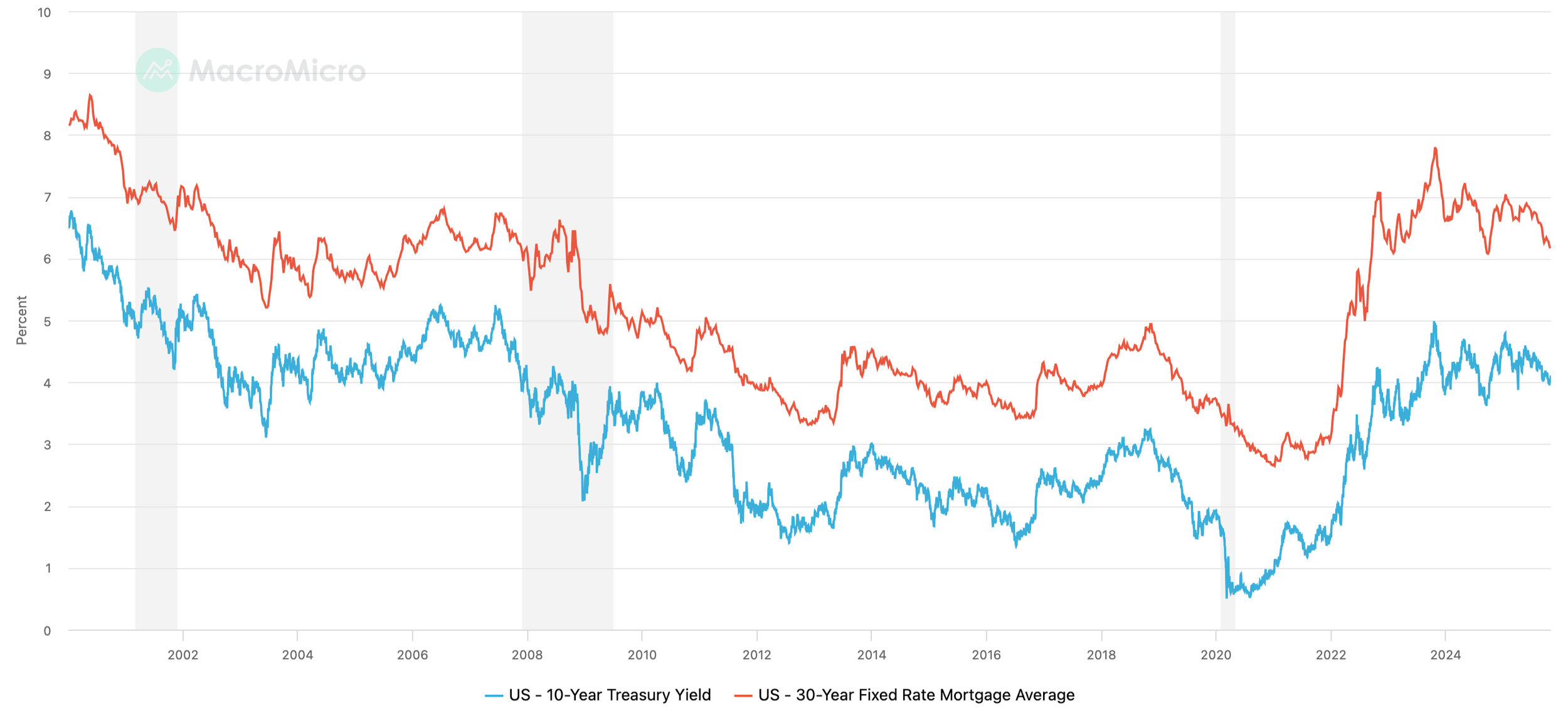

Mortgage Rates Track the 10-Year Treasury Yield

10-Year Treasury vs. 30-Year Fixed Rate Mortgage (2000-Present) | Courtesy of MacroMicro

Mortgage rates move based on long-term bond market expectations, and the single biggest benchmark is the 10-Year U.S. Treasury yield

Investors who buy mortgages (via mortgage-backed securities) expect a return competitive with something safe - and the 10-year Treasury is considered one of the safest investments in the world.

Typically, mortgage rates sit ~1.5% - 2% above the 10-year Treasury yield, because:

Mortgages have more risk than U.S. Treasuries

Investors want a premium to take on that risk

Mortgage-backed securities compete with Treasuries for investment dollars

So when the 10-year yield rises or falls, mortgage rates tend to follow - regardless of Fed announcements.

Why Rates Rose After the October 2025 Fed Cut

Here’s where it gets interesting — and where psychology matters more than policy; The rate cut was expected. Investors had already assumed a 0.25% cut was coming. That means it was already priced in to mortgage rates well before the meeting.

Jerome Powell’s comments changed expectations

What really shook the market wasn't the cut itself — it was the uncertainty Fed Chair Jerome Powell expressed in a speech after the announcement, about future cuts, specifically the one expected in December. Investors were hoping for another reduction, Powell suggested it may not happen, and suddenly, the outlook shifted.

Markets react to expectations — not events

Mortgage rates are set weeks (even months) ahead of Fed decisions. They don’t move based on today’s action — they move based on what investors believe will happen next.

So when Powell signaled hesitation, markets reacted: 10-year Treasury yields rose and mortgage rates followed

A bit of good news: Even with the bump, rates remain near their lowest level since 2022 (~6.17%).

The “Bird in the Hand” Principle

As I shared recently:

Mortgage markets favor certainty. “A bird in the hand is worth two in the bush” couldn’t be more accurate here.

Investors would rather have a known number today than gamble on the future. When expectations shift - even slightly - mortgage rates respond fast.

What This Means for Buyers & Sellers

If you’re waiting for the perfect moment, the market may never make that call for you.

A smart strategy looks at the full picture:

Current rates (still attractive historically)

Housing supply in your target neighborhood

Your personal timeline and financial goals

The opportunity cost of waiting:

Higher rates = more interest paid

Lower rates = faster appreciation and more competition

Of course, there is more to consider than rates alone - and strategy beats timing every time.

Ready to Make a Move in the DMV?

Whether you're upsizing, downsizing, or relocating - context matters, and so does timing. Let’s look at your goals, the current market, and craft the right plan together.